Credit cards are one of the most dangerous financial products ever invented for young people.

They are also one of the most useful.

Both of those sentences are true, and that is the whole confusion. A credit card in the hands of someone who understands the rules is a quiet little money machine — cashback, free flights, fraud protection, the start of a strong credit score. A credit card in the hands of someone who does not understand the rules is a trap that can take a decade to climb out of.

I want to give you the rules. Five of them. Memorize these and you will get all the perks without the pain.

How the trap actually works

Before the rules, you need to see the trap clearly. Most young people who get burned by credit cards do not get burned because they were reckless. They get burned because nobody ever explained how the math actually works.

Here is the math.

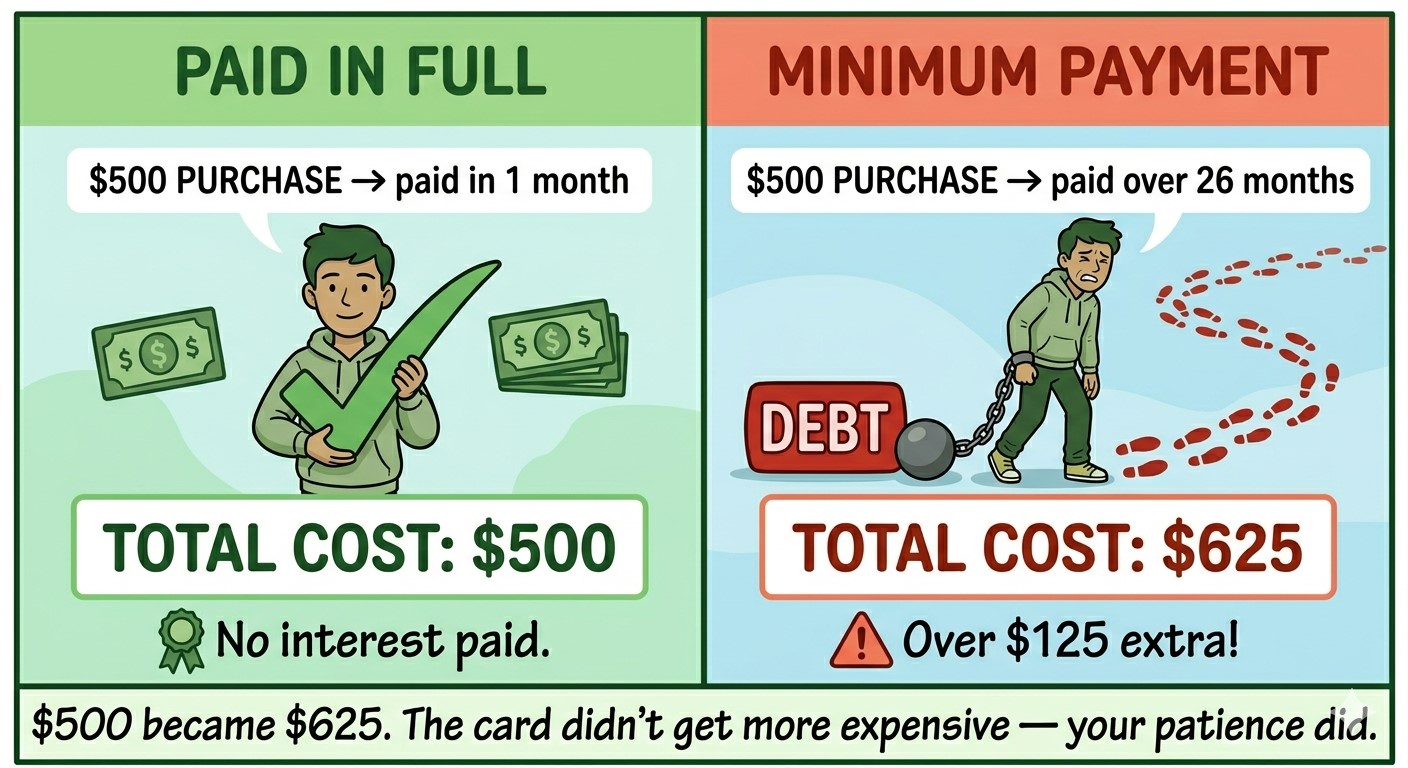

You buy something for $500. You pay the minimum payment — say $25 a month. Sounds responsible. But that card is charging you 22 percent interest a year on whatever you haven't paid yet. Most of your $25 each month goes to interest, not the actual $500.

How long does it take to pay off that $500 at minimum payments?

Twenty-six months. And you will have paid about $625 for a $500 purchase.

That is the trap. And it is designed to look small. The minimum payment is set deliberately low so the balance lingers and the interest keeps stacking. Credit card companies do not make money when you pay your bill in full. They make money when you don't.

Now to the rules that keep you on the right side of that math.

Rule 1: Pay the full balance every single month. No exceptions.

This is the most important rule. The other four are details.

If you can't afford to pay the full balance at the end of the month, you can't afford the purchase. That is not a judgment — it is just the math telling you something honest. The card is not free money. It is a 30-day loan that turns into a 22-percent loan if you don't pay it back.

The simplest way to follow this rule: set up an automatic payment for the full statement balance from your checking account, every month. Most credit card sites let you do this in about 60 seconds. Set it once, forget about it, and you will never accidentally fall into the trap. Ever.

Rule 2: Treat the card like a debit card

Here is the mental flip that protects you. A debit card spends money you already have. A credit card spends money you promise you will have at the end of the month.

If you would not buy something with your debit card today, do not buy it with your credit card today. The credit card is not an extra source of money. It is the same money, just shifted thirty days into the future — and only if you handle it right.

This sounds simple. It is the rule almost everyone forgets at 11 p.m. in front of a shopping site.

Rule 3: Get a card with no annual fee to start

There are credit cards out there with $95, $250, even $695 annual fees. These cards have great rewards, but they are not for beginners. For your first card, you want a no-annual-fee card that gives you 1.5 to 2 percent cashback on everything you buy.

A few solid options: the Citi Double Cash, the Chase Freedom Unlimited, the Wells Fargo Active Cash, or whatever similar card your own bank offers. All free to hold. All give you real money back on every purchase. Boring is good here.

Rule 4: Keep your balance under 30 percent of your limit

This one is about your credit score, which matters more than you think. Future landlords check it. Future employers sometimes check it. Future car loans and mortgages are priced based on it.

One of the biggest factors in your credit score is something called utilization — how much of your available credit you're using at any given time. If your card has a $1,000 limit and you charge $900, your utilization is 90 percent, and your credit score takes a hit even if you pay the balance off every month.

Keep your usage under 30 percent of your limit. If you have a $1,000 limit, try to keep your charges below $300 before each statement closes. If you need to spend more in a given month, just make a payment partway through to bring the balance down before the statement date.

Rule 5: Never take a cash advance. Ever.

Credit cards offer something called a "cash advance" — you can stick your card in an ATM and pull out cash. Don't.

Cash advances skip the normal grace period, meaning interest starts accruing the second you take the money. They also typically carry a higher interest rate than regular purchases. And they come with an upfront fee, usually 3 to 5 percent.

If you find yourself thinking about a cash advance, that is the universe telling you something has gone wrong with your money and you need to call a timeout. Use your emergency fund instead. That is exactly what it is for.

The reward for getting this right

Here is what happens when you follow these five rules for a few years.

You build a real credit score. You earn hundreds of dollars in cashback every year without lifting a finger. You get fraud protection on every purchase. You get a financial history that, when you turn 25 and want to rent an apartment or buy a car, opens doors for you instead of closing them.

And you pay zero interest. Not one dollar. Ever.

That is what a credit card looks like in the hands of someone who treats it like a tool. The card companies make a little money from the businesses you buy from. You get the perks. Nobody loses except the companies hoping you would forget to pay in full.

You will not forget. You set up the automatic full-balance payment in Rule 1. You are already ahead of 80 percent of cardholders out there.

If this resonates with you, this is one piece of a larger system. Money Matters walks through credit, debt, saving, investing, and building real wealth from your very first paycheck onward — in plain language, with worksheets that turn each idea into a plan you can actually follow.

Visit MoneyMatters.website to grab a copy of the book, download the free worksheets, and look around. The card companies are betting you won't read the fine print. Prove them wrong.

— William S. Baker