Here is something I wish someone had told me when I was 22.

Your money is not the enemy. It is also not just a number on a screen. It is the time you traded for it — the hours at the job, the early mornings, the days you said yes when you wanted to say no. Every dollar in your account has a story. It came from somewhere real.

How you treat that money — right now, whether you are in your late teens or your late twenties — sets the tone for the rest of your financial life. Not because the dollars themselves are huge yet. They are not. But because the relationship you build with money in these early years is the relationship you will keep for the next forty.

So let me say this plainly. If you treat your money well now, your money will treat you well later. Treat it carelessly, and you will spend the rest of your life chasing it. Treat it with respect, and it will quietly build a life you actually want.

What "treating money well" does not mean

Let me get one thing out of the way. Treating your money well does not mean living like a miser.

I am not telling you to skip your friend's wedding. I am not telling you to never go on a trip. I am not telling you to eat rice and beans for ten years so you can retire at 35 with a spreadsheet and no memories. That is not a life. That is a punishment.

The young people I worry about are not the ones who occasionally spend on something they love. They are the ones who don't notice their money leaving — who hit the end of the month, look at their checking account, and ask, "Where did it all go?"

That question — where did it all go — is the sound of money that wasn't respected. Not money that was overspent. Money that was spent without thinking.

The balance that actually works

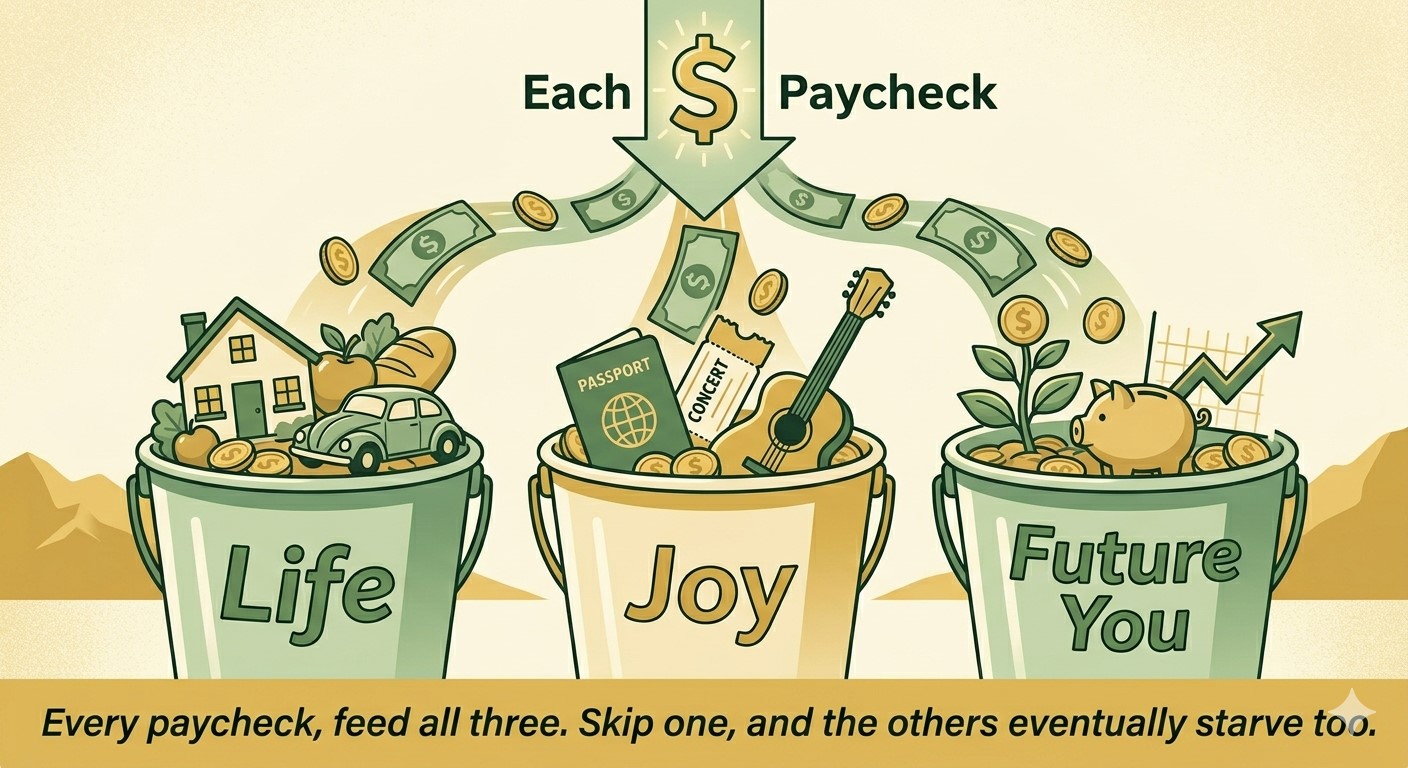

A healthy relationship with money lives in three buckets.

The first bucket is for your life. Rent, food, transportation, the bills that keep you alive. This is non-negotiable, and most of your money goes here, especially early on.

The second bucket is for joy. Real joy. A trip to a place you have dreamed about. A nice meal with someone you love. A concert you'll remember for twenty years. A guitar. A camera. Whatever lights you up. This bucket is not optional, and anyone who tells you otherwise is selling something. You are allowed to enjoy your life now — you should — but spend on the things that actually matter to you, not the noise.

The third bucket is for future you. The emergency fund. The 401(k) at work. The Roth IRA. The boring index funds that quietly grow in the background. This bucket feels invisible right now. It will not feel invisible when you are 45.

The trick is not picking one bucket. The trick is feeding all three, every single month, in proportions that fit your life.

The noise to skip

Here is where it gets honest. There are things young people spend money on that almost never look worth it five years later.

The car payment that takes up a third of your monthly income. The brand-new phone every year. The clothes you wore twice. The streaming subscriptions you forgot you had. The food delivery that costs three times what cooking would. The bar tab that disappeared in a fog.

None of these are wrong. I am not here to lecture you. But ask yourself, honestly: are these the things that bring you actual happiness? Or are they the things you bought because everyone around you was buying them?

There is a difference. Money spent on noise drains your account and brings you nothing. Money spent on meaning — on memories, on growth, on the people you love — pays you back forever.

The joys worth saving for

So what should you spend on, when the time comes?

Spend on experiences over things. A weekend in a city you have always wanted to visit will outlast any gadget. The gadget is in a drawer in two years. The trip is in your bones forever.

Spend on the people you love. A dinner with your parents. A gift that means something to your best friend. The wedding of someone you would not miss. Money used to deepen relationships is never wasted.

Spend on your own growth. A class. A book. A trip that teaches you something. A tool that helps you build something. These are not expenses — they are investments in the version of you that is still becoming.

Spend on health. Good food, a gym membership you'll actually use, a doctor visit you've been putting off, a therapist if you need one. These are not luxuries. They are the foundation everything else is built on.

These are the things worth saving up for, planning for, spending on with intention. The rest is mostly noise.

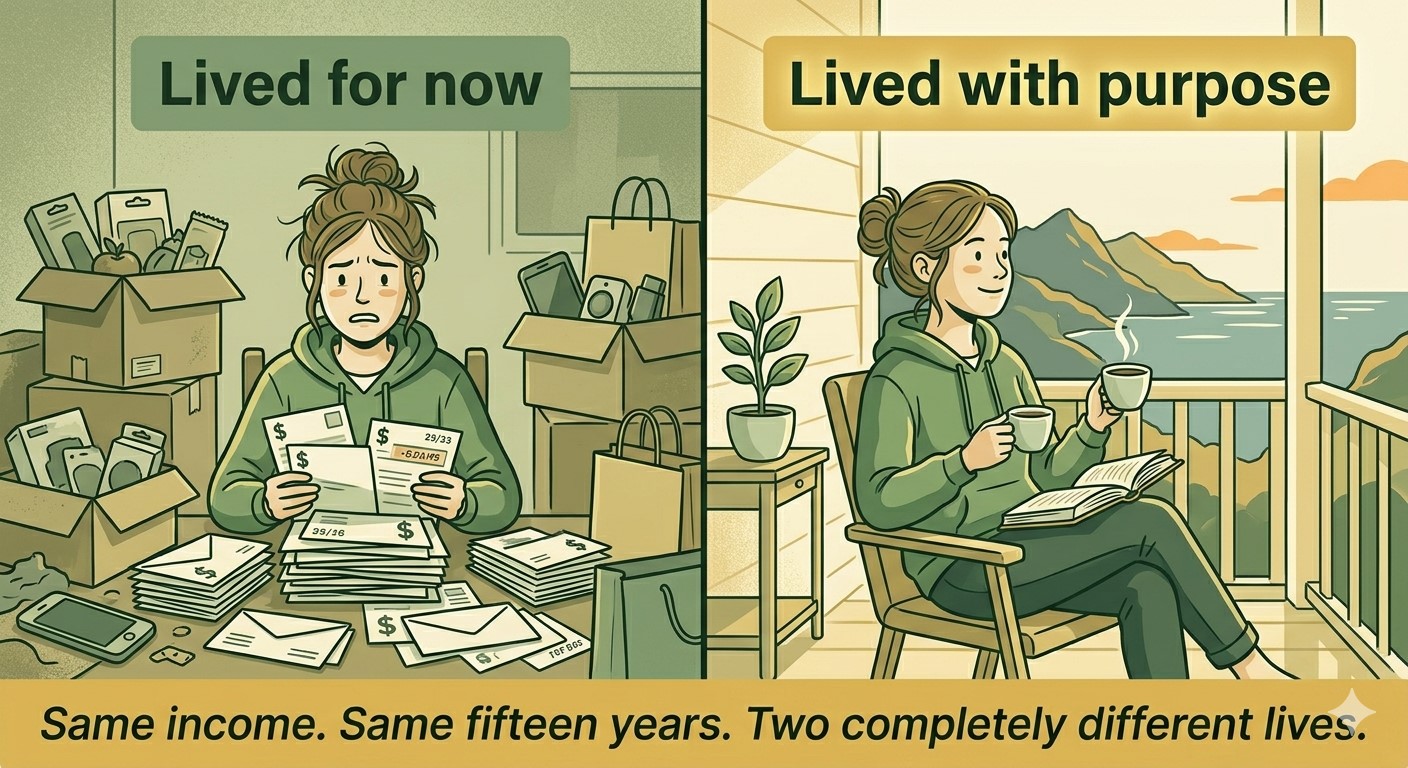

What happens when you do this for ten years

Here is the part that nobody believes when they are 22.

If you build this habit — feed your life, feed your joy, and steadily feed your future self — for just ten years, the math starts to work in your favor in ways that feel almost unfair.

Your emergency fund quietly grows into a real cushion. Your 401(k) starts looking like a number that surprises you. Your investments begin earning more in a year than you contributed to them. Compounding stops being a theory and becomes a thing that is actually happening to you.

And here is the magic part: you got there without giving up your life. You traveled. You spent on the things you loved. You showed up for the people who mattered. You just also, quietly, in the background, paid future you.

The respect part

So this is what I mean when I say to respect your money.

Respecting your money does not mean being afraid of it. It does not mean refusing to spend. It means remembering, every time you pull out your card, that the dollars you are about to spend came from your time. They are a piece of your life. Spend them on something worthy of that.

Sometimes that means saying yes to the trip. Sometimes it means saying no to the impulse buy. Sometimes it means moving $50 to your savings account before you even think about anything else. Always, it means being awake to the decision.

The young people who get this — even imperfectly — almost always end up free by their forties. Not rich, necessarily. Free. Free from the panic of a missed paycheck. Free to take the job they actually want instead of the one that pays the most. Free to give their kids the things they did not have. Free to do the work they care about, not just the work that pays the bills.

That freedom is not built in your forties. It is built in your twenties, one paycheck at a time, by people who decided early that their money was worth respecting.

You can be one of those people. The clock is already running.

If this resonates with you, this is exactly the philosophy that Money Matters is built on — the practical system for treating your money well, in plain language, with worksheets to put each idea into practice.

Visit MoneyMatters.website to grab a copy of the book, download the free worksheets, and look around. The way you treat your money this year is the life you live ten years from now.

— William S. Baker