Here is something nobody tells you when you are 21.

You are sitting on the single most valuable financial asset a human being can own. It is not a salary. It is not a degree. It is not even a windfall from a grandparent. It is something better, because you cannot buy it, and once you spend it you can never get it back.

It is time.

If you are 21 and you start investing $100 a month, you will end up with more money at 65 than someone who starts at 41 and invests five times as much. Not slightly more. Meaningfully more — even though they put in nearly three times the cash.

That sounds impossible. Let me show you why it is not.

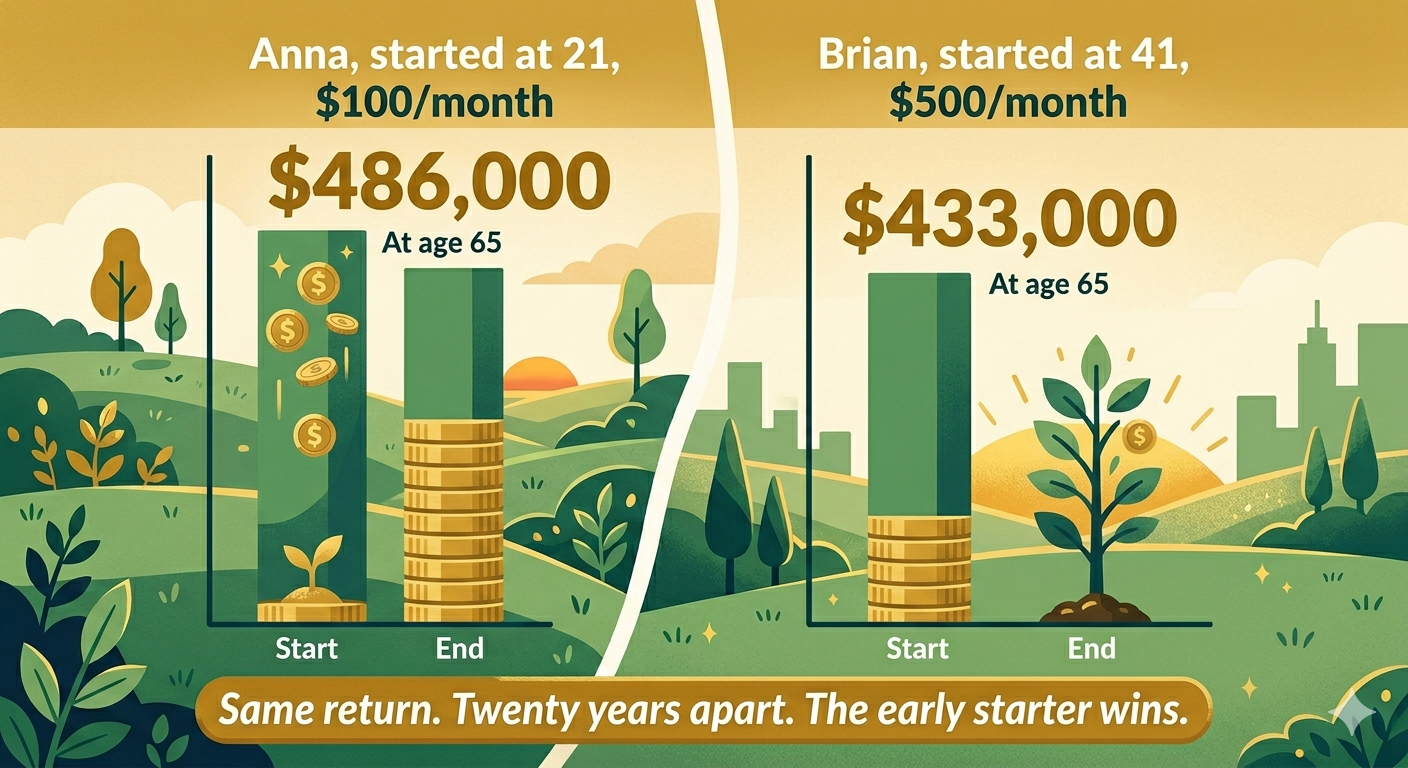

Meet two savers

Both of these people invest in the exact same boring index fund. Both earn about 8 percent a year on average — roughly what the U.S. stock market has returned over long stretches of history. Neither of them are stock pickers. Neither of them are geniuses. They are just regular people putting money in every month and leaving it alone.

Anna starts at 21. She invests $100 a month. She does this until she is 65. She never raises her contribution. She just shows up every month for 44 years.

Brian starts at 41. He invests $500 a month — five times what Anna ever did. He also keeps going until he is 65. He works hard. He hustles. He puts in way more money than Anna ever did, and for what feels like a long time.

Who ends up with more?

Anna ends up with about $486,000.

Brian ends up with about $433,000.

Brian invested $144,000 of his own money. Anna invested about $53,000. He put in nearly three times more cash. And he still finishes with $53,000 less than her.

That is not a trick. That is what 20 extra years does to money inside a compounding engine.

What is actually happening here

Compounding is just one idea, repeated over and over: your money earns money, and then that money earns money too.

The trouble is, in the first few years, compounding looks like nothing is happening. In year one, Anna invests $1,200 of her own money. She earns maybe $50 on it. Fifty dollars. If you only looked at year one, you would quit. Most people do.

But here is the thing. Anna does not quit. She keeps showing up, $100 at a time. By year five, her account has about $7,400 in it — and the market is starting to pay her real money on it. By year ten, the interest she earns in a single year is bigger than what she puts in. By year twenty, her money is making far more than she is. By year thirty, the original dollars she invested in her twenties are doing nearly all the work.

By the end, Anna has barely contributed anything in years 20 through 44 relative to what the market has earned for her. The money she put in when she was 22 is paying her rent at 64.

Brian never gets to that point. He runs out of years before his pile gets big enough to start doing the heavy lifting. He has to drag every dollar uphill himself, by hand. He never lets the snowball get going.

Anna's secret weapon was not income. It was time on the field.

The honest part

You probably do not feel rich at 21. You might have a part-time job, student loans, or zero savings to your name. Reading about compounding can feel like being shown a beautiful house you cannot afford to live in.

So let me say the honest part.

You do not need to invest $100 a month to start. You can invest $25. You can invest $50. The amount, in the early years, is almost beside the point. What you are actually doing when you start young is claiming the time. You are putting your flag in the ground and telling the compounding engine: the clock starts now.

Every year you wait, that flag moves forward. Every year you wait costs you more than the year before, because you are losing the most valuable years — the late ones, where the curve goes nearly vertical.

This is the cruel and beautiful symmetry of compounding. The early dollars feel small and almost pointless. The late dollars feel enormous and almost magical. They are the same dollars. The only difference is how much time you gave them.

What to do this week

Two things. Both small. Both will matter for the rest of your life.

1. Open a brokerage account. Fidelity, Vanguard, or Schwab. All free. All take about ten minutes. You do not have to put money in today. You just have to open the door.

2. Set up an automatic transfer. Even $25 a month. Send it to a broad index fund — a total stock market fund or an S&P 500 fund — and forget about it.

That is it. No timing the market. No watching the news. No checking your account every week. Just a quiet monthly transfer that runs in the background of your life for the next 40 years.

You will look up one day and realize the boring monthly transfer you set when you were 21 has quietly built the life your 65-year-old self gets to live in.

Your future self is begging you to start. Not because they want to be rich. Because they want to be free.

If this resonates with you, this is exactly the kind of thinking Money Matters was written to give young people early — when it still counts the most. The full system for how to invest simply, automatically, and without fear is laid out chapter by chapter, with the worksheets to put it all into practice.

— William S. Baker