Saving your first $1,000 sounds easy until you try it.

You make the decision. You feel motivated. You skip a few coffees, eat in for a week, maybe stash some money in a jar or a savings account. Two weeks later, life throws a tire repair at you, or a friend's birthday dinner, or a Saturday where the only thing that makes sense is takeout — and the money is gone again.

You start over. You quit again. You start to wonder if you're just bad with money.

You're not. The plan was bad. Specifically, the plan relied on willpower. And willpower, for everyone — for me, for you, for the financial advisor on YouTube — runs out around 8:30 on a Thursday night.

Here is what actually works.

The boring system

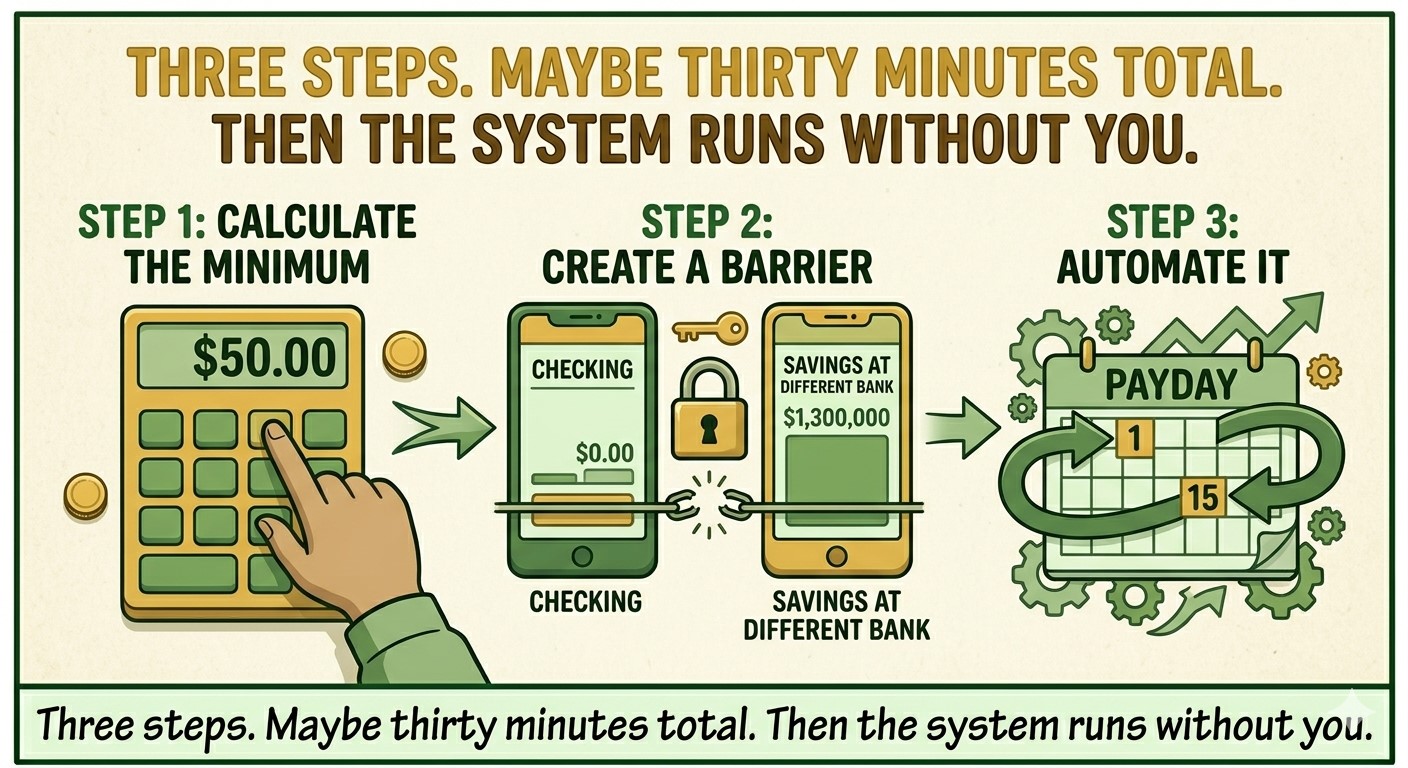

Forget the apps with the streaks. Forget the spreadsheet you'll abandon in February. The system that beats willpower every single time has three pieces:

1. Pick a number.

Not a dramatic number. A boring one. Look at one paycheck and decide what you can move out of your checking account without feeling it in the first 48 hours. Forty dollars. Sixty. A hundred. The exact amount matters less than you think. What matters is that you'll never miss it.

2. Open a separate savings account at a different bank.

Different bank — that part is important. If your savings sits in the same app as your spending money, you will spend it. Not because you are weak. Because it is right there. Different bank means an extra two clicks to get to it, and those two clicks are the friction that keeps the money alive.

A free online savings account at Ally, Marcus, or Capital One 360 takes about ten minutes to open. They also pay you real interest — currently around 4 percent a year — for the inconvenience of clicking twice.

3. Set an automatic transfer.

Same day your paycheck lands. Same amount, every time. Set it once and never look at it again.

That's the system. Not exciting. Not motivational. Doesn't require an app or a streak or a vision board. It just runs.

Why this works when willpower doesn't

When you save money "when there's some left over," you are asking yourself to make a hard decision every month at exactly the moment you have the least patience for it. End of the month, looking at what's left in your account, deciding whether to save it or keep it. You will lose that argument more often than you win it. Everyone does.

When you automate the transfer to happen first — the moment money arrives, before you've spent a dollar — you never have to decide. The decision was made once, weeks ago, when you were calm and thinking clearly. Every paycheck after that, the system does the work.

Pay yourself first. Make it automatic. Forget about it.

What if I can only save $25?

Save $25.

Save it every single paycheck for forty weeks and you'll cross the thousand-dollar line. That is not a long time. That is less than a year, and you'll have done it without trying.

Save $50 and you're there in twenty weeks.

Save $100 and you're there in ten.

The amount is just the dial that controls the speed. The thing that does the actual work is the system running in the background, automatically, while you live your life.

What that first $1,000 actually does

Here's the part most people miss: the $1,000 itself isn't really the point.

The point is what happens to your head while it builds.

Most young people live with a low-grade financial anxiety they don't even name — the feeling that one bad week, one car problem, one slow paycheck could blow up their whole month. That anxiety doesn't go away when your income goes up. It goes away when you finally have a thousand dollars sitting somewhere you can't easily touch.

When the alternator dies, you don't reach for a credit card. You reach for your savings. You pay it. You replenish it. You move on.

That is a different way of living. That is the difference between getting by and being okay. And it starts at $1,000.

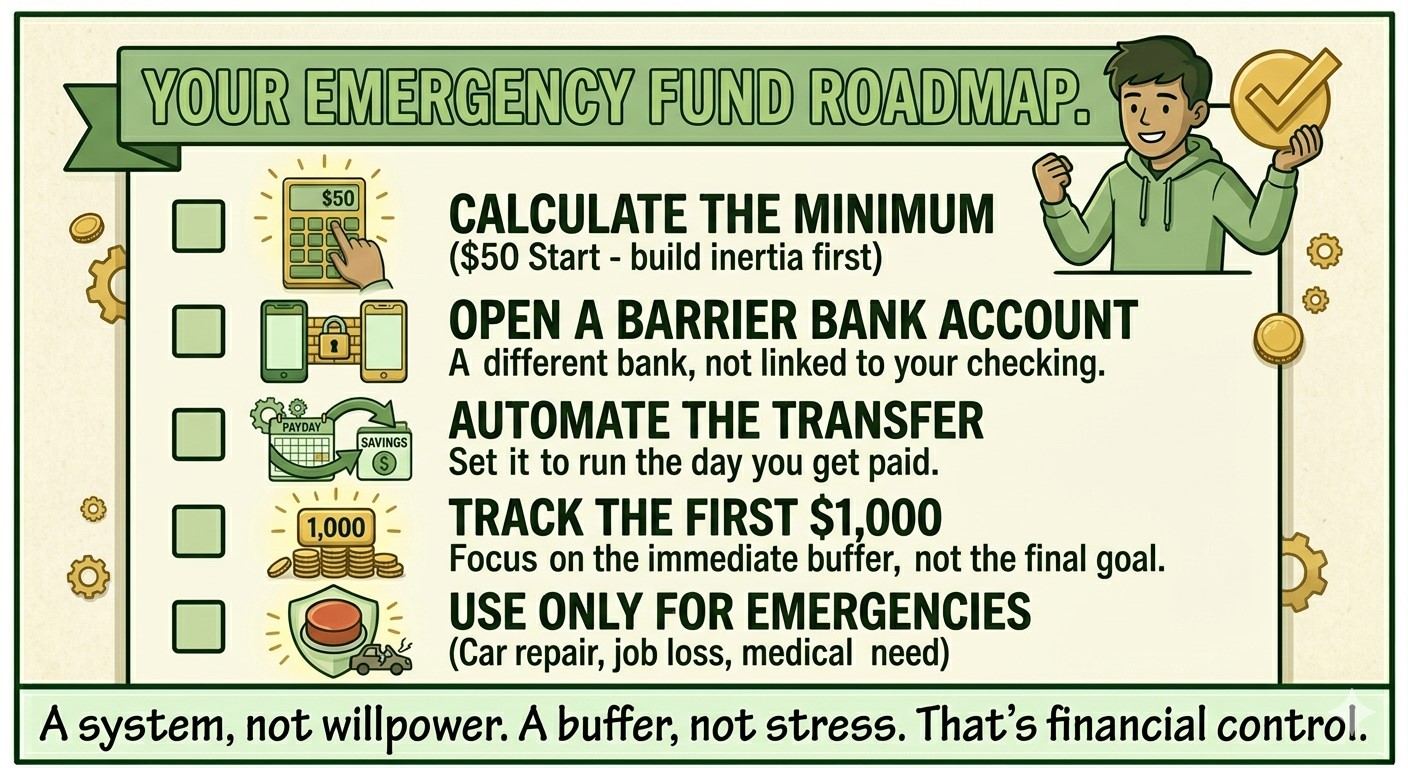

Start this week

Not next month. Not when the new year hits. This week.

- Pick an amount you won't miss.

- Open a separate savings account at a different bank.

- Schedule the automatic transfer to run the day your next paycheck arrives.

Three steps. Maybe thirty minutes total. And then the system runs without you, paycheck after paycheck, while your first $1,000 quietly builds itself.

If this resonates with you and you want the full system — the budget that doesn't feel like a budget, the three accounts every young person needs, the way to grow your savings rate without changing your lifestyle, and the worksheets to plan it all — that's exactly what I wrote Money Matters for. It's the money class you were never given, in plain language, designed for young people who want a real plan instead of more motivation.

Visit MoneyMatters.website to grab a copy of the book, download the free worksheets, and look around. The boring system is waiting on the other side.

— William S. Baker